By Alexander J. Wolf, Anthony P. DeLuca & Nicholas W. O’Brien, Koley Jessen

On August 15, 2020, Gov. Pete Ricketts signed LB 808 into law, introducing the Uniform Trust Decanting Act (UTDA) to Nebraska, with an effective date of November 13, 2020.(1) Nebraska now becomes the 10th state in the union to enact the UTDA, and one of 31 states to enact specific legislation relating to trust decanting. With local decanting legislation now on the books, Nebraska practitioners are likely eager to understand the potential uses, benefits, and risks of decanting.

More Efficient Modification

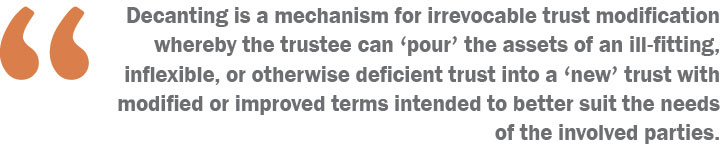

Decanting is a mechanism for irrevocable trust modification whereby the trustee can “pour” the assets of an ill-fitting, inflexible, or otherwise deficient trust into a “new” trust with modified or improved terms intended to better suit the needs of the involved parties. In the past, achieving such modification required judicial involvement, reliance on non-judicial settlement agreements, or the exercise of special powers of appointment. In this regard, decanting provides a streamlined (and likely more cost-effective) tool to achieve irrevocable trust modification.

Procedural Considerations & Implementation

Although the UTDA provides a clear and relatively concise roadmap, practitioners and fiduciaries must still adhere to best practices. Preparation of a formal resolution containing background information and recitals setting forth the specific decanting actions that will be taken, delivery of notice in accordance with the statutory requirements, and, in instances involving a second trust, careful effectuation of the asset transfers to be completed as part of the decanting process should all be carefully carried out. It should be noted that “private decanting”—that is, decanting without a requirement that notice is provided to the trust beneficiaries—is not permitted under Nebraska’s version of the UTDA.(2)

Additionally, the UTDA provides that a trustee’s discretionary authority will impact the extent of a fiduciary’s decanting power, so trust drafters should carefully weigh settlor intent with the impact that discretionary provisions may have on future ability to decant.(3)

Uses & Benefits of Decanting

Trust fiduciaries and beneficiaries in Nebraska will benefit from an increased ability to adapt to new norms in trust administration and changes in law. Looking broadly, trust decanting can be carried out to (i) change administrative provisions, (ii) further settlor intent, (iii) change or modify fiduciaries, (iv) divide, merge, or consolidate trusts, (v) correct scrivener’s errors or drafting ambiguities, (vi) modify beneficiary rights (e.g., accelerating or delaying distributions or eliminating mandatory income distributions), or (vii) add or eliminate powers of appointment.(4)

Tax Considerations & Limitations

Prior to decanting, a fiduciary should consider whether an exercise of the power may result in adverse consequences to the trust, its settlor, or its beneficiaries. While decanting will generally have no income tax consequences, decanting may cause meaningful gift, estate, and generation-skipping transfer tax consequences.

For example, decanting may cause a taxable gift if decanting results in a shift in beneficial interest of a trust’s beneficiary.(5) Further, decanting may trigger estate inclusion if a settlor is involved in the decanting in a way that evidences implied control over the trust assets.(6) Other parties to the trust may suffer negative estate tax consequences if such parties gain the ability to exercise powers includable in their estates as a result of the decanting.(7)

Particular caution should be exercised when a proposed decanting involves a generation-skipping transfer tax-exempt trust as decanting can, in certain instances, cause the trust to lose a portion or all of its generation-skipping transfer tax exemption.(8)

While the UTDA provides tax and estate planning practitioners—and the fiduciaries they represent—with increased flexibility to modify irrevocable trusts, the potential tax consequences of decanting necessitate careful, proactive consideration.

(1) Neb. Laws. 2020, LB 808; originally introduced as LB 902, but later amended into LB 808.

(2) But see Ariz. Rev. Stat. Ann. § 14-10819; Del. Code Ann. tit. 12, § 3528; N.H. Rev. Stat. Ann. § 564-B:4-419; Nev. Rev. Stat. § 163.556; S.D. Codified Laws §§ 55-2-15 to 55-2-21; Tenn. Code Ann. § 35-15-816(b)(27); W.S. 4-10-816(a)(xxviii), (b); N.H. Rev. Stat. Ann. § 564-B:4-419.

(3) See Neb. Laws. 2020, LB 808 § 21

(4) The authors note that caution should be exercised when modifying beneficial interests or adding or eliminating general powers of appointment as there can be unintended tax consequences.

(5) Cerf. v. Commissioner, 141 F.2d 564 (3d Cir. 1944) (holding that a beneficiary’s consent to a trust amendment eliminating the beneficiary’s income interest constituted a taxable gift when the amendment could not be completed without the beneficiary’s consent); see also Treas. Reg. §§ 25.2514-3(a) and 25.2514-3(c)(4).

(6) See I.R.C. § 2038.

(7) See I.R.C. §§ 2039, 2041, and 2042.

(8) See, e.g., Treas. Reg. § 26.2601-1(b)(4)(i)(D) and Treas. Reg. § 26.2601-1(b)(1).

Alexander J. “Alex” Wolf is a shareholder in Koley Jessen’s Estate, Succession, and Tax Department and is the president of the firm. Wolf’s practice focuses extensively on estate planning and estate administration, business succession planning, and organizational/tax planning for closely held businesses and nonprofit entities. He can be reached at alexander.wolf@koleyjessen.com.

Anthony P. DeLuca is a senior associate in Koley Jessen’s Estate, Succession, and Tax Department. DeLuca’s practice focuses extensively on post-death estate and trust administration where he counsels trustees and personal representatives on a variety of matters. DeLuca also provides proactive, comprehensive estate planning services ranging from basic estate plans to more complex wealth transfer planning and business succession planning. He can be reached at anthony.deluca@koleyjessen.com.

Nicholas W. “Nick” O’Brien is an associate in Koley Jessen’s Estate, Succession, and Tax Department. He provides services ranging from basic estate planning, business planning services, and trust and estate administration to wealth transfer techniques and counseling clients on charitable planning matters. He can be reached at nick.obrien@koleyjessen.com.

This story appears in 2020 Issue 6 of the Nebraska CPA Magazine.