By Sharon Kreider, CPA and Mary Kay Foss, CPA

At a Glance:

- Proposed regs clarify treatment of “excess deductions” at the termination of an estate or non-grantor trust.

- Conflicting instructions abounded for 2018 Forms 1041 K1 and 1040 Schedule A. Practitioners report even software vendors were muddying the waters.

- IRS response to conflict between instructions: “We’re working on it.”

- Proposed regulations clarify two items: administration expenses and excess deductions.

- The proposed regulations are very favorable.

Section 642(h) allows beneficiaries succeeding to an estate or trust property to deduct the carryover or excess if, upon termination, the estate or trust has: 1) a net operating loss carryover or a capital loss carryover; or 2) deductions for its last tax year that exceed gross income for the year—otherwise known as “excess deductions.”

Before the Tax Cuts and Jobs Act (TCJA), excess deductions on termination were passed out to residuary beneficiaries on a Schedule K-1, and then deducted by the beneficiary on Schedule A as a miscellaneous itemized deduction subject to the 2% of AGI limitation. In 2018, TCJA provided that miscellaneous itemized deductions subject to the 2% limitation were not deductible. If excess deductions are miscellaneous deductions subject to the 2% limit, then excess deductions are lost to our beneficiary. Can that be right? Or was it an unintended consequence of TCJA changes?

Conflicting Instructions. Someone read the instructions for the 2018 Form 1041 K-1 and the instructions for the 2018 Form 1040 Schedule A. The Form 1041 Schedule K-1 instructions directed the beneficiary to claim the excess deductions on Form 1040 Schedule A. The instructions for the 2018 Form 1040 Schedule A listed the miscellaneous deductions that were deductible (those not subject to the 2% limit). Excess deductions were not on the list. To confuse matters even more, practitioners reported that various software vendors were treating excess deductions differently. Some claimed a state deduction only; some were claiming a deduction for both federal and state; some were not claiming a deduction for either federal or state.

Tax Practitioner Planning. When the IRS was asked during the 2018 tax filing season how to handle the conflict between the Schedule K-1 instructions and the Schedule A instructions, they said, “We’re working on it.”

Existing Regs. Regulations for unused loss carryovers and excess deductions (§642(h)) were last updated in 1978. The examples date back to 1960 when neither the 2% limitation nor the passive loss rules were in the tax law. The existing regulations specify that the excess deductions are itemized deductions and are “not allowed in computing adjusted gross income.”

Proposed Regulations Clarify Two Items

Administration expenses. Proposed regulations (see REG-113295-18 at https://www.federalregister.gov/documents/2020/05/11/2020-09801/effect-of-section-67g-on-trusts-and-estates) clarify that the following deductions allowed to an estate or non-grantor trust are not miscellaneous itemized deductions subject to the 2% of AGI limitation:

- Costs paid or incurred in connection with the administration of an estate or non-grantor trust that would not have been incurred if the property were not held in the estate or trust are still deductible. These expenses include legal, accounting, and other administration costs specific to the estate or non-grantor trust.

IRS will continue to consider expenses listed in §67(b) and §67(e) as not miscellaneous itemized deductions. They are instead deductible in arriving at the AGI of an estate or non-grantor trust. - The deduction of those expenses is not affected by new §67(g), which provides for the suspension of the deductibility of certain miscellaneous itemized deductions for taxable years beginning after December 31, 2017, and before January 1, 2026.

Excess deductions. The proposed regulations issue guidance on determining the character, amount, and allocation of deductions over gross income succeeded by a beneficiary on the termination of an estate or non-grantor trust. These proposed regulations affect estates, non-grantor trusts (including the portion of an electing small business trust), and their beneficiaries.

During the final year of an estate or of a non-grantor trust, some of the excess deductions are deducted in arriving at AGI (above the line) and not from AGI (below the line). The §642 proposed regulations (which can be relied on for years beginning after December 31, 2017) divide excess deductions into three categories:

- deductions allowed in arriving at adjusted gross income,

- non-miscellaneous itemized deductions, and

- miscellaneous itemized deductions.

Note. The beneficiary that is allocated the deductions will be subject to any applicable limitations on their return. For example, the state and local tax (SALT) limitations may apply to the beneficiary.

Example. In an example from the proposed regulations, a residuary beneficiary can claim excess deductions on their individual income tax return as a deduction in arriving at the beneficiary’s AGI.

Assume that a trust distributes all its assets to B and terminates on December 31, Year X. As of that date, it has excess deductions of $18,000, all characterized as allowable in arriving at adjusted gross income under Internal Revenue Code Section 67(e). B, who reports on the calendar year basis, could claim the $18,000 as a deduction allowable in arriving at B’s adjusted gross income for Year X. However, if the deduction (when added to B’s other deductions) exceeds B’s gross income, the excess may not be carried over to any year after Year X.

Tax Practitioner Planning. One of the two examples in the proposed regulations is flawed because it treats property taxes on a rental as an itemized deduction instead of directly allocated to rental income. The example was an update of an example from 1960, which referred to §642(h) regulations in effect then.

Proposed Regulations Are Very Favorable

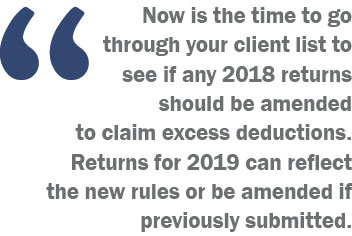

Now is the time to go through your client list to see if any 2018 returns should be amended to claim excess deductions. Returns for 2019 can reflect the new rules or be amended if previously submitted. If you are amending a 2018 or 2019 return, you may need more information from the trustee or tax preparer to break down the excess expenses into the three categories specified in the regulations.

Sharon Kreider, CPA has helped more than 15,000 California tax preparers annually get ready for tax season for the past 19 years. With a keen ability to demystify complex individual and business tax legislation, Kreider instructs Western CPE tax seminars and presents regularly for the AICPA, the California Society of Enrolled Agents, and A.G. Edwards. She gained her detailed, hands-on tax knowledge through her extremely busy, high-income tax practice in Silicon Valley.

Mary Kay Foss, CPA specializes in handling complex trusts and individual tax planning. She goes above and beyond the compliance work to understand the personal issues faced by her clients and how they affect retirement planning and trust administration and funding. In addition, she teaches classes for CPAs and other financial professionals about retirement planning and estate planning. Foss has 30-plus years of public accounting experience, providing planning and tax preparation services for complex estates, trusts, and individuals. She also works closely with fiduciaries to assist with trust funding and reporting to beneficiaries.

For more information, contact Western CPE’s customer service center at (800) 822-4194 or wcpe@westerncpe.com.

©2020 Mary Kay Foss & Sharon Kreider

This story appears in 2020 Issue 6 of the Nebraska CPA Magazine.