By Sharon Kreider, CPA

At a Glance:

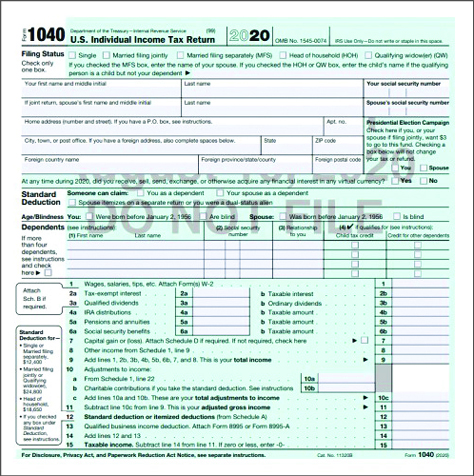

- The IRS released a draft of Form 1040 for the 2020 tax year.

- The form is not postcard-sized.

- Virtual currency has a new position.

- The CARES Act changed the reference point of charitable contributions.

- There will be a separate reconciliation schedule for stimulus checks—no instructions yet.

- The amount you owe may be more complicated due to line 37 (new for 2020).

The IRS released the draft of the 2020 Form 1040 (see https://www.irs.gov/pub/irs-dft/f1040–dft.pdf). It still doesn’t look like the Form 1040 in “the good old days.” And it’s still not (nor is it ever likely to be) a postcard. Here are a few changes to the 2020 form that you should note, particularly ones that are due to COVID-19 relief legislation.

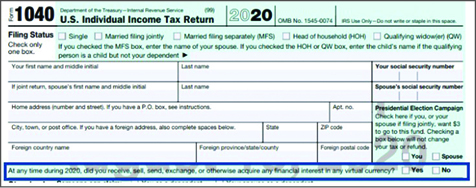

1. The virtual currency question has been moved from the top of Schedule 1, Form 1040 (see https://www.irs.gov/pub/irs-dft/f1040s1–dft.pdf), to the front page of the Form 1040, right after the “Presidential Election Campaign” checkboxes. According to the IRS, only a few more than 800 returns reported virtual currency transactions in 2014 and 2015. The IRS was suspicious of that number and added the virtual currency question to the 2019 tax return, making us effectively the enforcers of their reporting campaign.

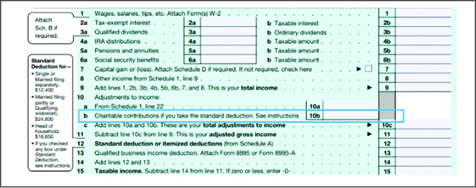

2. Line 10b was added to the front page of the Form 1040 for “Charitable contributions if you take the standard deduction. See instructions.” CARES added cash contributions up to $300 as an above-the-line deduction, but only for those claiming the standard deduction.

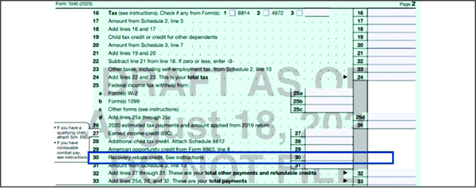

3. On page two of Form 1040, federal withholding tax has been divided into three entries: Line 25a for W-2 withholding, Line 25b for Form 1099 withholding, and Line 25c for other withholding.

4. On page two of Form 1040, Line 30 has been added to report the “Recovery rebate credit. See instructions.” The instructions have not been released, but it appears there will be a separate reconciliation schedule/form where any excess credit over the amount received in mid-2020 as an advance will be calculated and carried over to line 30.

Example. Pat and Chris had a baby in 2020. They are entitled to a $2,900 Recovery Rebate Credit. They received an advance of $2,400 in June 2020. When they file their 2020 tax return, Chris and Pat are entitled to a $500 credit on Line 30.

5. On page two of Form 1040, Line 37 has been added. “Schedule H and Schedule SE filers, line 37 may not represent all of the taxes you owe for 2020. See Schedule 3, line 12e, and its instructions for details.” What does this mean? It’s the CARES Act’s deferral of the employer’s share of 2020 OASDI payroll taxes. While CARES calls the new provision an “employer deferral,” the deferral also applies for part of self-employment tax. The new line 12e on Schedule 3, Form 1040 (see https://www.irs.gov/pub/irs-dft/f1040s3–dft.pdf), says “Deferral for certain Schedule H or SE filers (see instructions).”

Example: Stephanie has $100,000 of 2020 net self-employment income. The OASDI portion of her self-employment tax is $11,451 ($100,000 x .9235 x 12.4%). Stephanie is entitled to defer the “employer” share of her OASDI tax, or $5,726. The deferred amount is due 50% on December 31, 2021, and 50% on December 31, 2022.

6. Line 12b has been added to Schedule 3, Form 1040 (see https://www.irs.gov/pub/irs-dft/f1040s3–dft.pdf), to enter “Qualified sick and family leave credits from Schedule(s) H and Form(s) 7202.” The Families First Coronavirus Response Act (FFCRA) requires small employers (fewer than 500 employees) to provide paid sick leave and family leave for employees affected by COVID-19. The employer receives an offsetting credit against their payroll tax deposits. Self-employed individuals are eligible for sick leave and family leave. Their refundable credits are claimed on the self-employed individual’s 2020 Form 1040 Schedule 3, Line 12b. For details on the sick leave and family credits, see the IRS FAQs at https://www.irs.gov/newsroom/covid-19-related-tax-credits-for-paid-sick-and-paid-family-leave-overview.

Sharon Kreider, CPA

For more information, contact Western CPE’s customer service center at (800) 822-4194 or

wcpe@westerncpe.com. © 2020 Sharon Kreider

This story appears in 2020 Issue 5 of the Nebraska CPA Magazine.