By Nathan Patterson & Alex Wolf, Koley Jessen

With the 2020 election right around the corner, the United States may be on the precipice of another major tax regime overhaul. Just as quickly as President Trump’s 2017 Tax Cuts and Jobs Act (TCJA) brought the estate and gift tax exemption to its all-time high, the election of Joe Biden and a swing to a Democrat-controlled Senate could push the exemption back to pre-2017 levels, or perhaps even lower. As discussed in more detail below, tax and financial advisers serving high-net-worth individuals should take this time to examine the desirability for some of their clients to utilize their remaining exemption during the 2020 tax year. Moreover, with the potential that any tax law changes passed next year could have a retroactive effective date of January 1, 2021, it is important that these discussions take place as soon as possible. Put simply, high-net-worth clients who wish to “lock in” the use of their exemption should be prepared to do so by December 31, 2020, or they could potentially lose out on millions of dollars of estate and gift tax savings.

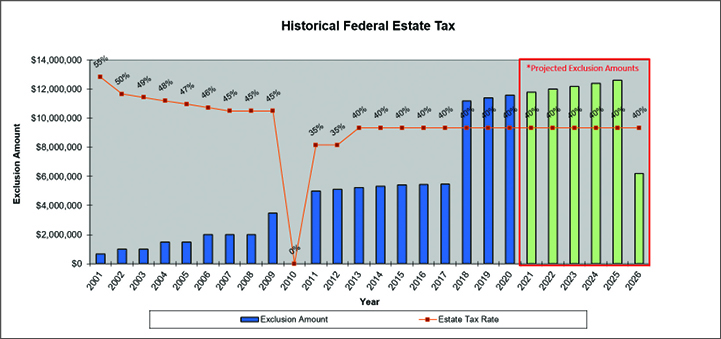

By way of background, the estate and gift tax systems work hand in hand to tax the value of all assets that may be transferred from an individual during life and at death in excess of the exemption. As of January 1, 2020, the exemption allows each individual to pass up to $11.58 million tax free to their desired beneficiaries, either at the time of death or through lifetime gifts. To the extent lifetime gifts and gross estate value on a combined basis exceeds the exemption amount, a tax rate of 40% applies. The exemption amount and tax rates have changed over time and at the turn of the 21st century started with an exemption level as low as $600,000 and an effective tax rate of 55%. The chart above provides context into the historical exemption levels as well as the respective tax rates over that time.

The passage of the TCJA doubled the exemption and brought it to its current all-time high. Absent congressional intervention, the estate and gift tax exemption is set to remain at $11.58 million (adjusted each year for inflation) until 2026, at which point, the exemption will sunset and drop back down to pre-TCJA levels (approximately $6 million after inflation adjustments). High-net-worth individuals will need to make lifetime gifts to others or in trust prior to the 2026 sunset to take full advantage of the increased exemption levels. Individuals who fail to utilize the increased exemption prior to the sunset will lose out on a minimum of $2.4 million in estate tax savings.1 However, with the 2020 election, it may be a good time for high-net-worth individuals and their tax and financial advisers to reevaluate whether lifetime gifts should be made not just prior to the 2026 sunset, but prior to the end of 2020.

In the 2020 presidential race between Biden and Trump, two very different tax landscapes are at issue. As discussed above, Trump’s TCJA nearly doubled the exemption to its current level, and, if reelected, those levels will likely stay on course to sunset in 2026. If Biden is elected, however, his tax plan could drastically lower the exemption amount much sooner than otherwise anticipated. Currently, it is believed that a Biden administration will push to return the estate tax rules to “historical levels,” which would likely mean an exemption of anywhere from $3 million to $5.5 million, and a tax rate of 50% to 55%. The earliest a bill could be passed to effectuate these changes would be sometime in 2021, but, with the pendulum potentially swinging in favor of Democrats in the Senate, it is believed that such a bill could be made effective retroactively to January 1. This means that if Biden is elected, exemption levels could potentially drop by at least $6 million effective January 1, 2021, and any high-net-worth individuals who do not utilize the exemption prior to that date would lose out on the estate and gift tax savings associated with the drop (i.e., this would mean a minimum of $2.4 million less in assets passing to their beneficiaries based on the current 40% rate).

With this potential change in mind, it is imperative for tax and financial advisers of high-net-worth individuals to relay the importance of examining whether it would be desirable to use their exemption before year end through lifetime gifts. These lifetime gifts may be made directly to others or in specially designed trusts intended to carry out specific tax and practical objectives. With the baby boomer generation set to pass on the largest levels of wealth in history, many high-net-worth clients will likely benefit from a serious discussion about the foregoing. However, with a potential deadline of December 31, 2020, to avoid the risk of retroactive effectiveness of any bill passed after the election, time is quickly running out to begin these discussions and implement any planning. t

1 ($12 million (approximate exemption level prior to sunset) – $6 million (approximate exemption level post sunset)) x 40% (estate and gift tax rate) = $2.4 million in estate tax savings

Nathan Patterson is an attorney in the Estate, Succession, and Tax Department at Koley Jessen. He provides services ranging from basic estate planning, business planning, and tax strategies to wealth transfer techniques and high-net-worth estate planning. With hands-on experience operating and managing a family farm, he also provides “boots on the ground” expertise to agriculture clients and family businesses on planning matters specific to the ag industry. He can be reached at nathan.patterson@koleyjessen.com.

Alex Wolf is a shareholder in Koley Jessen’s Estate, Succession, and Tax Department and is the president of the firm. Wolf’s practice focuses extensively on estate planning and estate administration, business succession planning, and organizational/tax planning for closely held businesses and nonprofit entities. He can be reached at alexander.wolf@koleyjessen.com.

This story appears in 2020 Issue 5 of the Nebraska CPA Magazine.