In a memorandum decision1 released on Dec. 30, 2025, the Tax Court addressed a number of issues related to a late-filed federal estate tax return. Among the issues addressed by the court is the liability of an estate residue transferee for the estate’s unpaid estate tax deficiency, failure to file penalty, and accuracy-related penalty.

The court first reviewed the liability of the estate for the deficiency and the penalties. Having relatively little difficulty agreeing with the IRS on the majority of the substantive estate liability issues, the court then turned to the potential liability of the estate residue distributee and to the burden of proof.

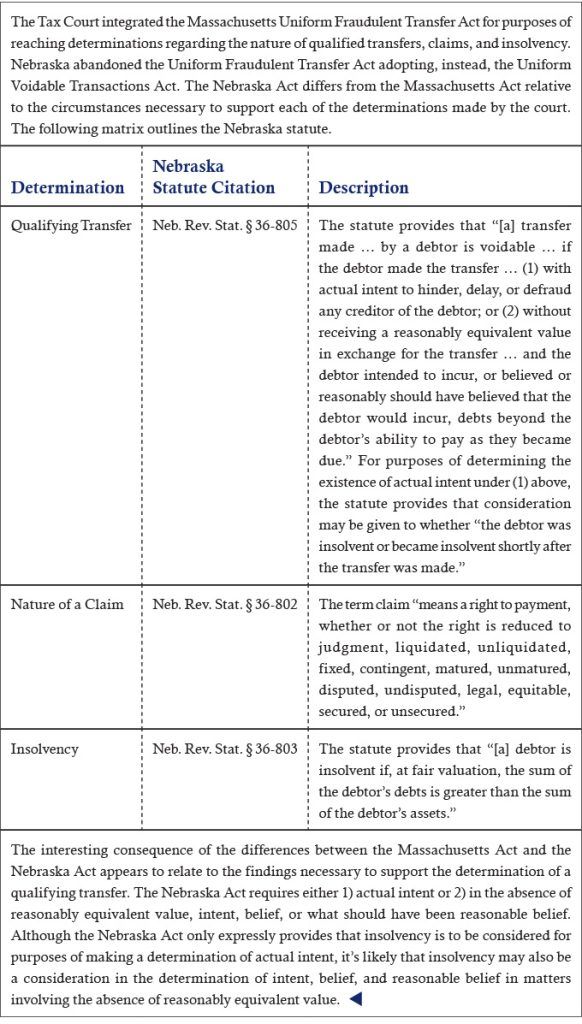

Relative to the transferee liability question, IRC § 6901 provides that the IRS may assess and collect liabilities related to estate taxes from a “transferee of property.” It also provides that the period of limitations with respect to the assessment of such liability against the initial transferee is one year after the expiration of the limitation period for the assessment against the transferor. Finally, IRC § 6901 provides that the term “transferee” includes 1) a donee, heir, legatee, devisee, and distributee and 2) with respect to estate taxes, any party that is personally liable pursuant to the special wealth transfer tax lien statute.2 Relative to the burden of proof question, IRC § 6902 provides that the IRS bears the burden of proof to establish that a party is liable as a transferee of property.

Noting that as a result of the transferee liability statute, the IRS is placed in “precisely the same position as that of ordinary creditors under state law,” the court turned to the relevant state fraudulent transfer act. Since the applicable state law “is the law of the state in which the transfer occurred” and since the transfer occurred in Massachusetts, the court reviewed the Massachusetts Uniform Fraudulent Transfer Act. The court cited the Massachusetts Act relative to the nature of transfers it reaches, as follows:

A transfer made … by a debtor is fraudulent as to a creditor whose claim arose before the transfer was made … if the debtor made the transfer … without receiving a reasonably equivalent value in exchange for the transfer … and the debtor was insolvent at the time or the debtor became insolvent as a result of the transfer.

The court also cited the Massachusetts Act relative to the meaning of the term “claim.” A claim is “a right to payment, whether or not the right is reduced to judgment, liquidated, unliquidated, fixed, contingent, matured, unmatured, disputed, undisputed, legal, equitable, secured, or unsecured.”

The court found that the deficiency arose at the time the return should have been filed. It also found that, as a result of the distribution of the estate residue, the “estate made the transfer without receiving equivalent value and held no assets after the transfer.” Noting that a debtor is insolvent if the sum of its debts is greater than the fair market value of its assets, the court concluded that transfer of the estate residue rendered the estate insolvent and that the transfer was therefore fraudulent within the meaning of the state statute. As a result, said the court, “the IRS may seek to recover the state’s tax liability from [the residue transferee].”3

The case is an interesting demonstration of the occasional interaction of state and federal statutes. It’s also an important reminder of the potential liability that transferees bear for unpaid estate taxes.

Bryan Robertson is a trust services director for FNBO, where he works as part of a team to deliver a wide range of complex estate and trust planning and administrative services. He is also an adjunct assistant professor of accounting for Nebraska Wesleyan University, where he has taught an income tax course every fall semester and a corporate income tax course every spring semester since 2014. As a member of the Nebraska Society of CPAs for 34 years, Robertson is a past chairman of the Society and presently serves on the Fall Conference Committee. You may reach him at (402) 602-8769 or bryanrobertson@fnbo.com.

- Estate of Georgia M. Spenlinhauer, T.C. Memo. 2025-134 (December 30, 2025).

- The special wealth transfer tax lien statute, IRC § 6324, provides that a transferee who receives property included in the gross estate, to the extent of the value of that property at the date of the decedent’s death, is personally liable for unpaid estate tax liabilities.

- Presumably as a result of the inclusion in IRC § 6324(a)(2) of the phrase “to the extent of the value,” the IRS acknowledged that the transferee’s liability is limited to the value of property actually received by that transferee.