A. Steps for “F” Reorganization

For purposes of this explanation, we will use the following terms:

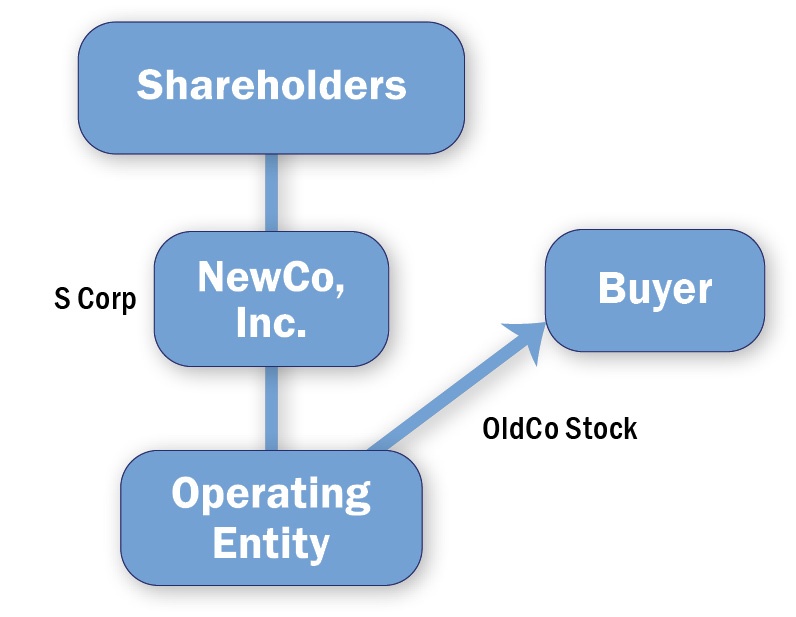

- Operating Entity – This refers to the original entity, which is taxed as an S corporation.

- NewCo – This is the new entity, which will become the holding company of the Operating Entity.

- QSub – This refers to a “qualified subchapter ‘S’ subsidiary” as defined in Section 1361 of the Code.

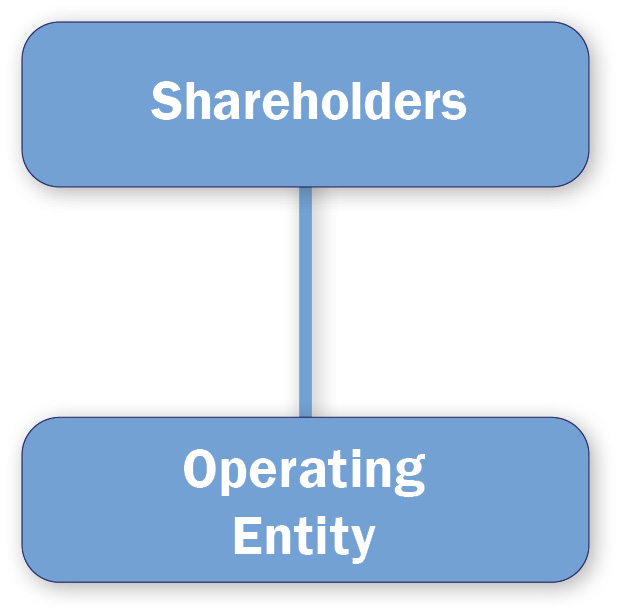

The starting point may look like the following:

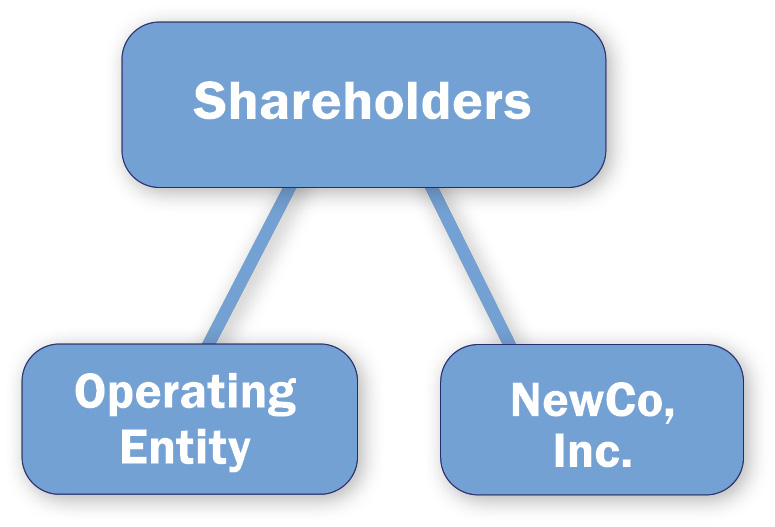

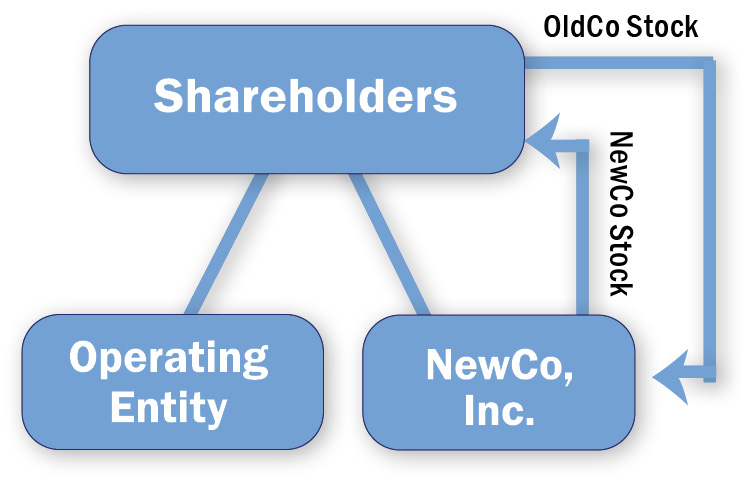

Second, the same owners contribute all of their equity in the Operating Entity to NewCo in exchange for ownership interests in NewCo.

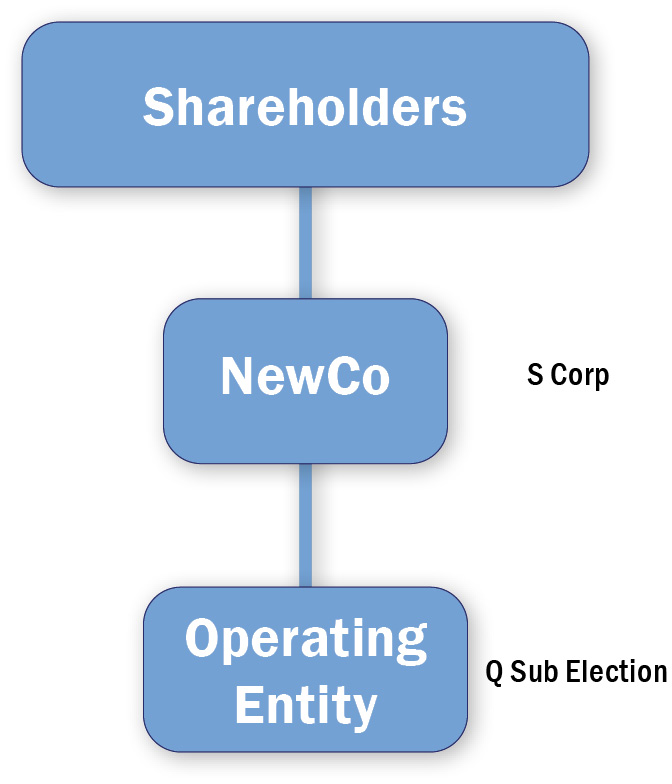

Third, immediately following the contribution, NewCo causes the Operating Entity to elect to be taxed as a qualified subchapter S subsidiary (“QSub”). This is an important step, the complexity of which is frequently overlooked.

After the above steps are completed, NewCo should cause the Operating Entity to convert from a state-law corporation to a state-law limited liability company.3

Following such conversion, an entity investor could then purchase equity interests of the Operating Entity without disqualifying the S election of NewCo. Upon such a purchase, the Operating Entity, of course, would no longer be an eligible QSub.

Because the limited liability company is a disregarded entity for income tax purposes, the purchase would be treated as an acquisition of assets of the limited liability company by the Buyer. Following the purchase, the limited liability company would be characterized as a partnership under the “check-the-box” rules. For example, if the Buyer acquires 70% of the interests of the Operating Entity, NewCo will recognize gain or loss as if NewCo had sold 70% of the assets of the Operating Entity to the Buyer.

B. Documentation

These steps must be memorialized in a written Plan of Reorganization, which would also specify the business purpose of the reorganization. Each party must file a required statement with their respective return under the Treasury Regulations for the tax year, which requires a report of the names and EINs of all parties to the reorganization; the date of the reorganization; and the aggregate fair market value of the assets, stock, or securities of the Operating Entity transferred in the reorganization.

C. Qualification as an “F” Reorganization

- All of the stock4 of NewCo must be distributed in exchange for equity interests of the Operating Entity.

- The same persons must own all of the equity interests of the Operating Entity immediately prior to the reorganization and of NewCo immediately after the reorganization, in identical proportions.

- NewCo may not hold any property or have any tax attributes prior to the reorganization.

- The Operating Entity must completely liquidate for federal income tax purposes in the reorganization but it is not required to dissolve under state law. This could include a deemed liquidation under the Section 7701 Regulations.

- Immediately after the reorganization, no entity other than NewCo may hold property that was held by the Operating Entity immediately before the reorganization, if the other entity would succeed to the tax attributes.

- Immediately after the reorganization, NewCo may not hold property acquired from anyone other than the Operating Entity, if NewCo would succeed to the tax attributes.

D. Carryover of the S Election

E. Carryover of EIN

IRS guidance provides that, if carried out properly, the Operating Entity will retain its original EIN. This allows the Operating Entity to utilize the same business registrations and other aspects associated with its unique EIN. NewCo must apply for a new EIN.

F. Tax Results

If structured properly, the follow tax results apply:

- No gain or loss is recognized on the transaction by the Operating Entity.

- No gain or loss is recognized by the owners of the Operating Entity (at least until a subsequent sale of the equity of the Operating Entity). The owners’ basis in the equity interests of NewCo will be the same as the basis they had in their equity interests of the Operating Entity. The holding period for the equity interests of NewCo will include the holding period of the Operating Entity equity interests.

- No gain or loss is recognized by NewCo on its receipt of assets in exchange for its equity interests (until a subsequent event such as a sale). NewCo succeeds to all tax attributes of the Operating Entity under Section 381(c).

Again, there are many traps for the unwary, but an “F” reorganization can be a useful tool for restructuring an entity taxed as an “S” corporation prior to certain investments or acquisitions. Practitioners should follow the above steps and assure compliance with all aspects of Section 368(a)(1)(F) as well as the various forms required to be filed with the IRS.

Hannah Fischer Frey and Jesse Sitz are partners at Baird Holm LLP, focusing their law practices in the areas of federal and state income tax law and business succession planning. Fischer Frey and Sitz work closely with other tax practitioners and preparers to document and structure deals for their clients in a tax-efficient manner.

For more information, contact them at hfrey@bairdholm.com and jsitz@bairdholm.com, respectively.

1This article refers to “S corporations” generally to refer to limited liabilities companies or corporations that have made an “S” election under Section 1361 of the Code. Under the check-the-box rules, a multi-member limited liability company can elect taxation other than its default partnership status.

2For purposes of this article, the term “corporations” when used in the phrase “S corporations” is intended to reflect the tax status of the entity, not the entity’s state law entity form.

3If the Operating Entity is already a limited liability company, this step may be skipped. Note, however, that complexities apply relating to a limited liability company making a QSub election. Special attention should be given to the election forms required for such an election.

4For purposes of this article, the term “stock” when used in the phrase “S corporation stock” is intended to refer generally to ownership interests of an entity taxed as an “S” corporation.

5With that said, there are nuances related to the tax election forms to be filed during the reorganizations that would apply to limited liability companies, but not state-law corporations. Care should be taken to ensure that the proper forms are filed with the Internal Revenue Service.