CPE Catalog & Events

Offering quality, affordable education to fit your career goals, learning style, and schedule.

CPE Catalog & Events Read More »

Offering quality, affordable education to fit your career goals, learning style, and schedule.

CPE Catalog & Events Read More »

Robert A. “Bob” Helm 1940-2025Nebraska Certificate #0852Society Certificate #059457-Year MemberNESCPA Chairman, 1986 | Distinguished Service to the Profession Award, 1991 Kevin P. Hitchcock 1976-2025Nebraska Certificate #9688Society Certificate #68523-Year Member Terry R. Johnson 1941-2025Nebraska Certificate #2955Society Certificate #226140-Year Member Eric J. “Ric” Ortmeier 1945-2025Nebraska Certificate #1286Society Certificate #093944-Year Member Duane R. Polodna 1957-2025Nebraska Certificate #2724Society Certificate

Membership in the Nebraska Society of CPAs signifies your commitment to the accounting profession and the belief that much can be accomplished by working together. Welcome to the premier organization for CPAs and accounting professionals in Nebraska.

Welcome New Society Members Read More »

Bernard W. “Bernie” Auten, CPA, shareholder of Auten Pruss & Beckmann PC in Norfolk, has been recognized by Cedar Rapids Public School for his “generous donations, unwavering commitment, and tireless dedication” to the district. As a result, the new Riverside gymnasium floor in Cedar Rapids, Neb., will be dedicated to Auten, who is a 1967

Members in the News Read More »

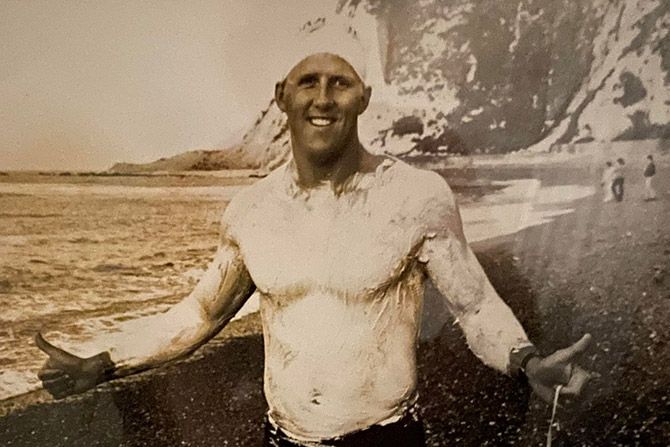

In the heartland of America, where the plains stretch wide and the nearest coastline is more than 900 miles away, one man has charted a course that defies convention. Kristian “Kris” Rutford, a seasoned CPA based in Lincoln, Neb., has not only navigated the complexities of tax codes and financial statements but has also conquered some of the most challenging open-water swims in the world.

Balancing Ledgers and Laps The Extraordinary Journey of Kris Rutford

Read More »

In January 2025, a new CEO of the American Institute of CPAs and Association of International Certified Professional Accountants took the reins from long-time leader Barry Melancon, CPA, CGMA.

Q&A With AICPA’s New President & CEO Mark Koziel, CPA, CGMA Read More »

From time to time, owners will ask us if they need to sign a noncompete agreement. The answer stays the same: “Yes, Yes, Yes. Buyers will always want a noncompete.” An essential part of every practice sale/purchase is the noncompete clause or, as it is sometimes called, the covenant not to compete. This clause or agreement is essentially a protection for the buyer that spells out what a seller cannot do regarding performing accounting, tax, and related services after the sale.

Don’t Go There The Agreement That Tells You What You Can’t Do

Read More »

In an increasingly global world, Nebraska’s philanthropic spirit remains rooted in something enduring: place. For decades, individuals and businesses in our region have chosen to give locally, not just because it feels good, but also because it works.

Philanthropy That Stays Local Read More »

Today we hear a lot of debates in political circles where someone on the political spectrum is contending that an action by the Executive Branch (typically the President) is not constitutional. These debates are most often not whether a statute is constitutional, but whether the action by the Executive Branch is unconstitutional in how it exercises the authority under statute. We are not weighing in on these debates. Instead, the purpose of this article is to highlight how we are often able to identify where a state department of revenue or county board taxing authority has applied a statute in an unconstitutional way.

Section 1361 of the Internal Revenue Code sets forth the requirements for an entity electing to be taxed under Subchapter S as an S corporation. S corporations continue to be a popular choice due to the potential savings on self-employment taxes resulting from the bifurcation of payments made to the owners into wages versus distributions, subject to certain requirements.